The Seasonality of Investing

Why good opportunities - like good mangoes - rarely last forever

I hope everyone is enjoying the best of the season. Here in the Western world, where I now live, spring finally seems to have arrived - we’ve even had 3–4 genuinely hot days already.

Back in India, where I grew up, it’s mango season. And nothing beats mango season. Nothing beats Indian mangoes, either. Banganapalli any day for me, in case you’re wondering.

- Wikipedia")

Part of the joy of a mango lies in its incredible taste and juiciness. But a large part of the charm is also its fleeting nature. Good mangoes - like the Banganapalli - have a short season. It begins around April and lasts perhaps two to two-and-a-half months at most. Outside that window, the alternatives are never quite the same.

That cyclicality is what makes mangoes special. And even a casual mango connoisseur will tell you that nothing mango-flavoured ever comes close to the real thing.

Why am I talking about mangoes?

Partly because it is mango season. But also because, like mangoes, truly good investing opportunities tend to arrive in cycles.

“Good,” of course, is subjective here.

It doesn’t take a lot of rocket science to see that many of the investments I hold - value-oriented businesses with steady, boring growth trajectories, defensible positions, and reasonable valuations - are not exactly in vogue right now.

And yet, most of these businesses continue to deliver solid underlying results. One would normally expect stock prices to eventually reflect that reality. But apart from a couple of exceptions - Sumitomo Corporation and Crocs, Inc. come to mind - many others continue to languish.

Meanwhile, the market is clearly chasing two things:

AI

Everything adjacent to AI winners

Having spent the last several months skilling up on AI myself, I can absolutely see the transformative potential. I also understand why so many people are excited - and in some cases fearful or anxious - about what AI could do to the business world.

And to be clear, I think many AI investments will work out extremely well over the medium to long term.

Anthropic, for instance, has emerged from relative obscurity over the past year to establish itself as one of the most credible players in the AI tooling ecosystem. It isn’t publicly traded, but its private valuation has risen dramatically - and probably for good reason.

That said, I also believe not everything currently being labelled an “AI winner” will ultimately deliver the business results implied by today’s valuations. And conversely, not everything currently treated as an AI loser will remain a loser forever.

If that’s the broad backdrop, then what’s the best way to manage a portfolio through it?

My answer is probably some combination of personal preference, temperament, and circumstance.

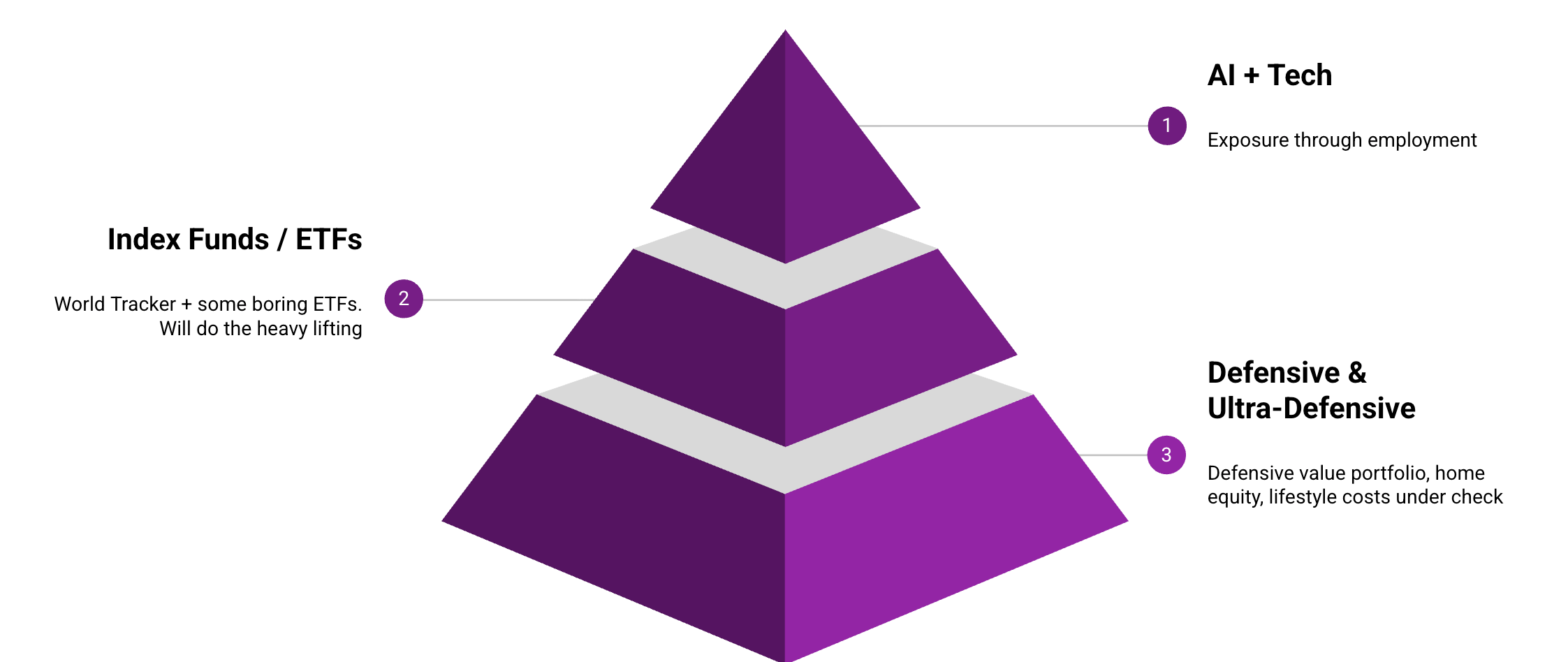

Firstly, I work at a tech company that is heavily leveraging AI across its business operations. We’ve also repositioned ourselves as an AI company. If the AI wave continues to compound from here, the equity I hold in my employer will likely appreciate meaningfully over time. That alone gives me meaningful exposure to the upside.

Secondly, I’ve always been fairly honest with myself about my own limitations as an investor. Because of that, I continue to keep a significant portion of my capital in ETFs and index funds - with the majority sitting in the Vanguard FTSE All-World tracker.

That means that as the broader equity market continues its bull run - whether powered by AI today or by something entirely different tomorrow - I still participate in that upside. At the same time, keeping things diversified at a global index level rather than concentrating heavily into AI or tech gives me a reasonable hedge if sentiment eventually reverses.

Thirdly, as an individual stock picker, I have always leaned defensive and somewhat contrarian. I spend far more time thinking about downside protection than upside maximisation.

That approach has done two things for me over the past decade-plus:

It has allowed me to sleep well.

It has made me enough money to comfortably beat inflation while preserving flexibility.

Keeping my portfolio relatively defensive has also meant that whenever life presented other opportunities - investing in a business venture, buying a house, or simply taking a different risk elsewhere - I was financially prepared to act.

And then there’s the ultra-defensive layer: a home I live in, where every mortgage payment slowly but steadily reduces leverage on the books, coupled with a conscious eye on lifestyle inflation. Both reduce the pressure to constantly chase outsized investment returns.

Loosely speaking:

(1) is leveraged AI exposure,

(2) is hedged momentum exposure,

and (3) is defensive contrarian investing.

Will this be the best-performing asset allocation at every point in time? Almost certainly not.

Will it help me achieve my long-term financial goals while letting me sleep peacefully at night?

Most likely, yes.

A quick programming note before I wrap up: after a fairly quiet Q1 and an even quieter April, I’ve started becoming slightly more active again on the investing front. I’m also hoping to find the time to write a bit more regularly in the coming months.

So stay tuned for more.

And with that - happy investing.

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is for educational and entertainment purposes only. Do your own due diligence before investing. I may hold or enter into positions in the securities mentioned above. This is not a solicitation to buy or sell any security.