Tariff Special: Harley Davidson (NYSE:HOG)

Tariffs, Buybacks, and a Potential Value Play

At the time of drafting this, the world of business, as well as the stock markets, is being rocked by the introduction of tariffs by the US. The markets have responded through a significant sell-off. In the midst of this chaos, is there something worth picking up? I analyse one such opportunity.

![Harley Davidson Ride Experience [UK] - Virgin Experience Days](https://substackcdn.com/image/fetch/$s_!uk3e!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F18321ef0-f2d6-4acc-a4bd-78dc62419d96_1200x800.jpeg "Harley Davidson Ride Experience [UK] - Virgin Experience Days")

Harley-Davidson, Inc. is an iconic American motorcycle manufacturer known for its heavyweight, cruiser-style bikes and strong brand heritage. Founded in 1903 in Milwaukee, Wisconsin, the company has built a global reputation for quality craftsmanship, distinctive V-twin engines, and a loyal rider community. In addition to producing motorcycles, Harley-Davidson offers parts, accessories, and apparel while also operating a financial services division. The company continues to evolve with new technologies and electric models like the LiveWire, balancing its legacy with innovation in the modern motorcycle market.

I am not a big motorcycle fan, and you might never see me on a Harley-Davidson, but that won’t stop me from analyzing what I think might be a somewhat interesting setup.

At the time of finalising this draft (Friday afternoon) - the stock is trading at its 52-week low and has a P/E of 6.23 - it is trading close to it’s pandemic-crash low, a period during which the stock has almost exclusively above where it is today. This stock was mentioned in a podcast as a possible tariff loser, so I jumped in to see what I could learn from it.

The Financials

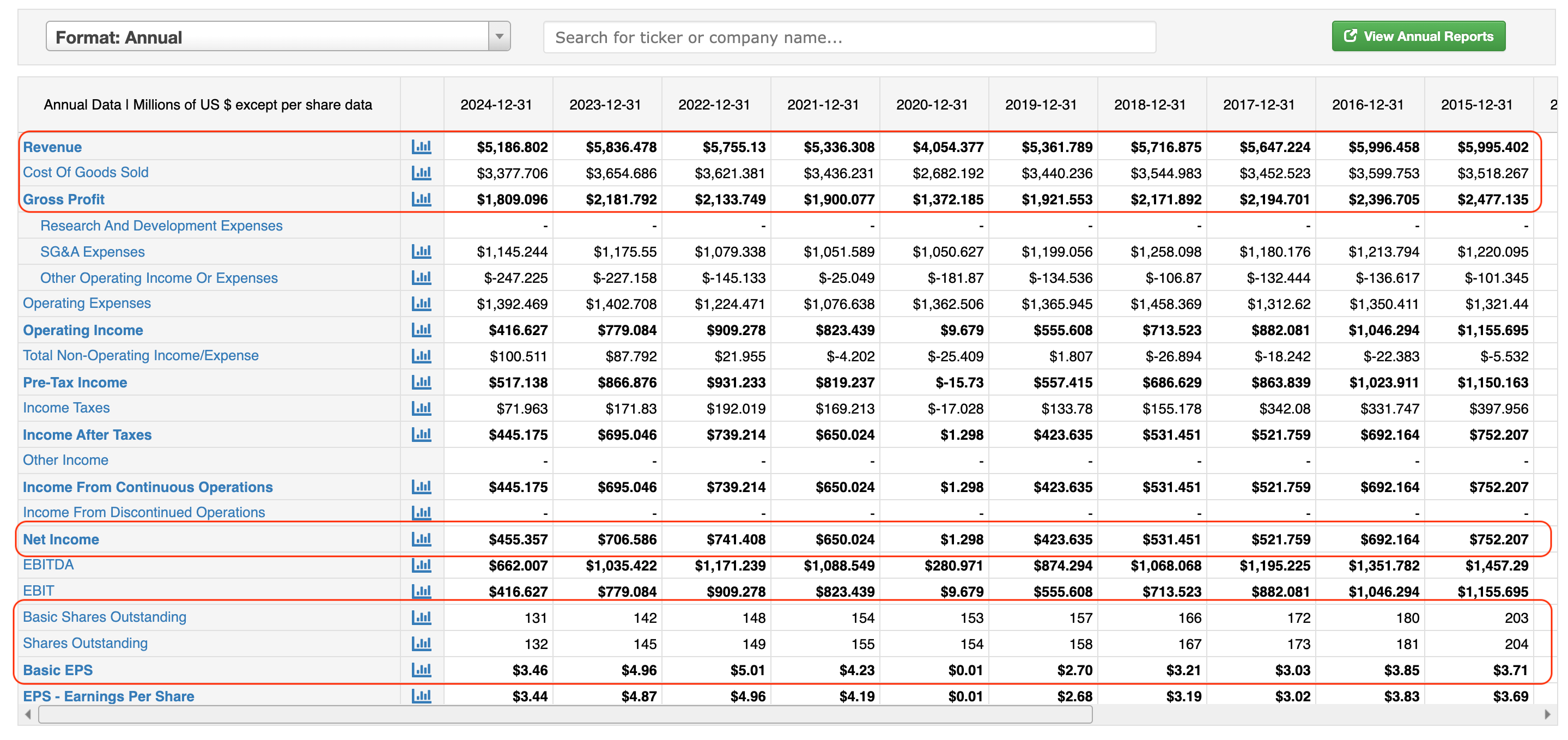

Let’s look at the business. Here is a quick glance at its long-term financials.

Leaving aside the year of the pandemic, the company consistently has a revenue of ~$5Bn and has produced anywhere between $400Mn and $700Mn of profit in any given year. Sure, it doesn’t seem to have any growth characteristics, but it has also never produced a loss, even during the pandemic year.

Pay special attention to the outstanding shares line—the company has been reducing its stock count as if its shares are going out of fashion, burning away a third of its outstanding shares in the past 10 years. Maybe there’s a cash flow problem? Let’s look at that too.

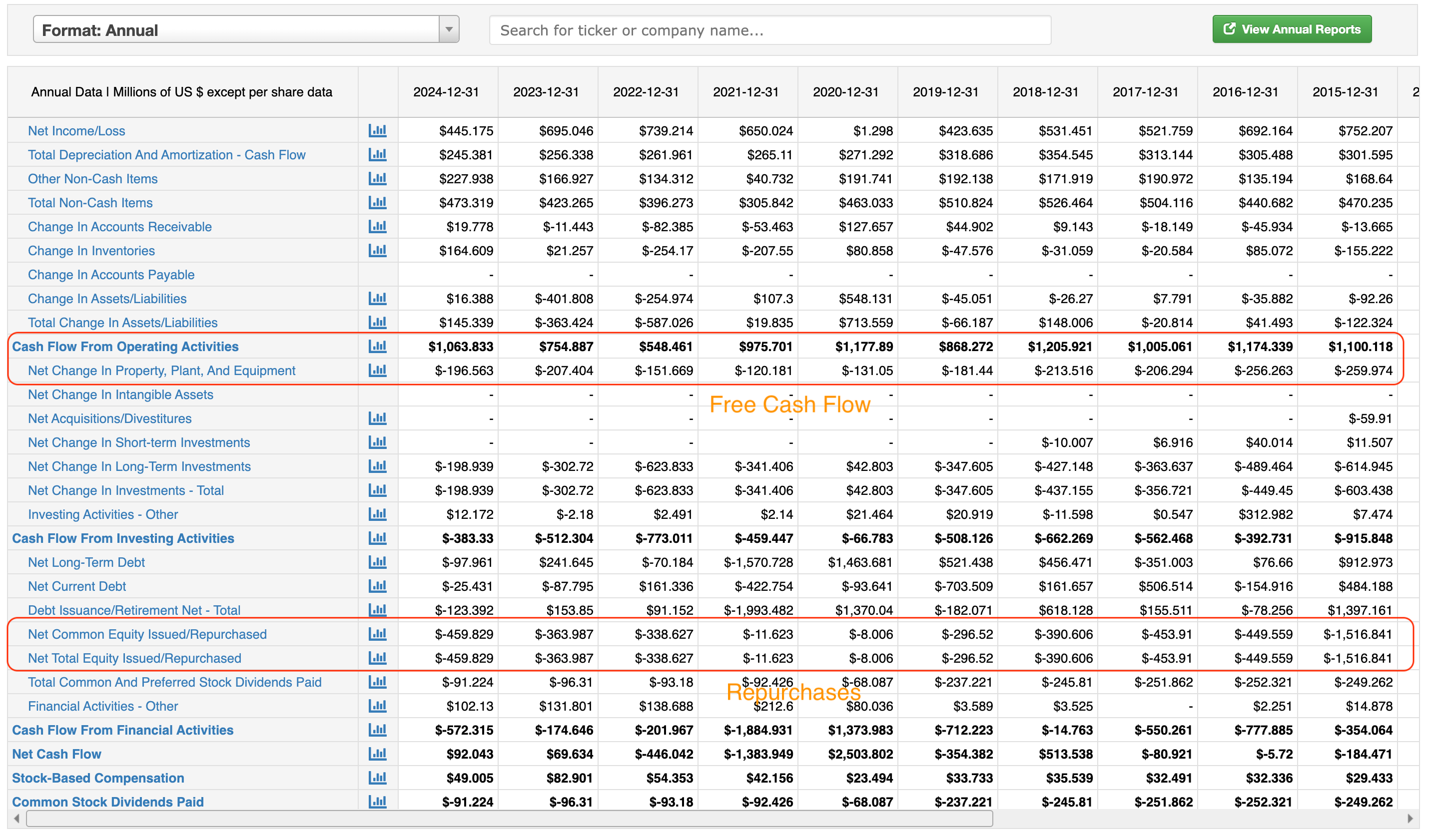

The company is consistently generating free cash flow of $600Mn to $800Mn (again, excluding the pandemic year) and has been deploying it consistently to repurchase stock—almost averaging $450Mn a year. With an average EPS of $3.75 over the past 10 years and the stock being priced at no more than $50, but more often between $30 and $40, management is effectively retiring outstanding shares at between a 7x and 15x P/E. And they are absolutely on the right path. It is a far better use of money than anything else, at least for long-term, ongoing shareholders. Now, let’s examine the balance sheet.

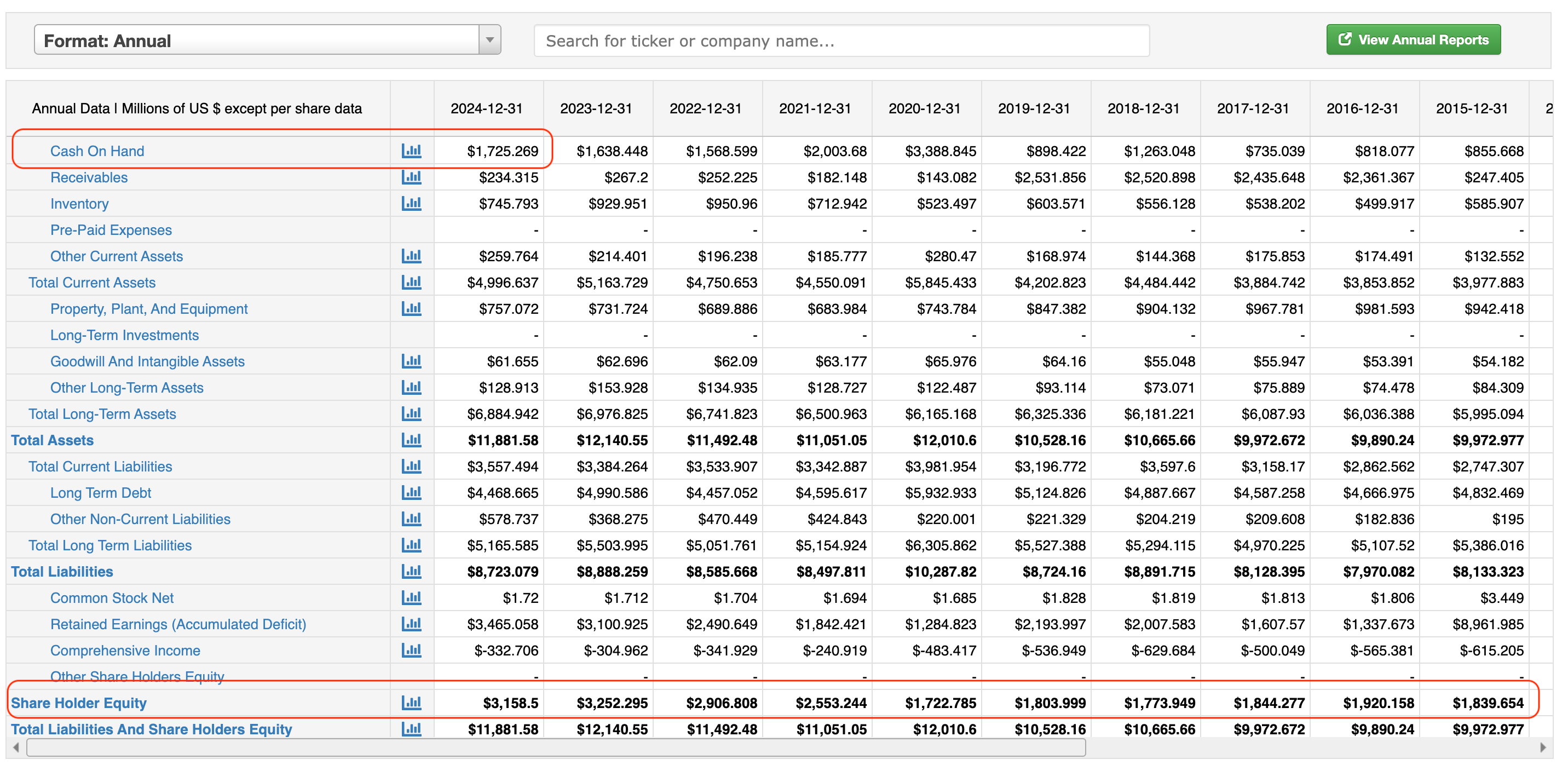

The company holds $3Bn in shareholder equity, with goodwill (the accounting make-believe number) being less than 2%. They also have $1.6Bn in cash on their books—of course, cash needs to be considered in line with other current assets and current liabilities, but even net current assets stand healthily at $1.2Bn. The company’s board has authorized up to $1.1Bn in share repurchases starting in Q4 2024 and lasting through the end of 2025. Of that, only $250Mn was deployed in Q4 2024, and the company has already guided for up to $350Mn in share repurchases in 2025, though I reckon it could deploy a lot more cash if the price continues to be depressed.

The HOG in the Shop

So why is the stock so depressed today? The announcement of tariffs seems to be the biggest factor—fears that U.S. tariffs will be reciprocated by the rest of the world, particularly the EU, which could impact sales in those regions. For instance, Canada and the EU account for about a fifth of its sales. Harley-Davidson’s overall market share stood at 37.3%, lower than in the past. The narrative goes: "Harley-Davidson is losing market share brand, a fifth of its sales are under threat from retaliatory tariffs around the world, which will put pressure on margins." This all seems plausible.

The flip side is that all but one of Harley-Davidson’s competitors in the U.S. market are foreign, and they will all face tariffs coming into the country. To be fair to the markets, stock of Polaris (NYSE:PII), their main domestic competitor, has also been punished in recent days, but their decline seems systemic, as it has lost two-thirds of its value in the past year.

One way to look at this is: what happens if 50% of EU + Canada sales disappear? That would mean a gross profit reduction of about $180Mn. Assuming only a third of that can be recovered in operating costs, we’re talking about a $120 million hit to the bottom line. That puts us at about $300Mn in net income. Assuming the company clears 15% of the stock as promised, we’re looking at ~$2.80 in EPS, which would still put the stock at under a 8x P/E.

As long-term investors, we need to consider the following:

Will the U.S. tariffs stick? (Quite probable at the moment.)

Will the tariffs attract retaliatory tariffs from other countries? (Uncertain.)

What will be the impact of both U.S. tariffs and retaliatory tariffs on total revenue? (Relatively measurable.)

Where does that leave us? (Still in reasonable territory.)

Summary

To summarize, we have a company with a strong brand name and stable but non-growing revenue that generates a relatively solid amount of profits and cash flow. This cash flow is being prudently returned to shareholders via dividends and share repurchases. The company faces some headwinds due to geopolitical events, but we can make reasonable assumptions about those as we go along. The stock trades at a mere 6.2x EPS today, and if the company continues to retire 10-12% of its market cap through repurchases this year, depending on how things unfold in the coming years, the current valuation could range between 6x and 10x P/E on future earnings. At some point, this will trigger an inflection in the stock price.

In the midst of what has been a spectacular run in stocks overall, opportunities like this with a reasonably good margin for safety and conservative pricing for a company with strong capital allocation record are rare. While I outline my reasons for optimism, investing always carries risk, so I won’t be betting the farm anytime soon. However, slow and steady accumulation might be the way to go - I have already picked up a small position through $23 strike, January 2027 call options and I have initiated positions in the stock itself, but I will likely add to my position by buying the stock outright in small lots here and there.

As always, happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.