Summary Analysis: Bunzl Inc

Summary Analysis: Bunzl Inc

A bolt-on acquisition expert

After my last post on Sumitomo Corporation (8053.T), let’s move westwards and talk about Bunzl Inc, a UK headquartered distribution services business.

Founded originally in 1854, Bunzl spent its first century in existence in various businesses completely unrecognisable from its current existence - as a haberdashery, as a cigarette and filter maker, as a paper and pulp company and even a brief foray into data processing. Somewhere in 1980 they pivoted into the world of distribution, which is what it resembles today.

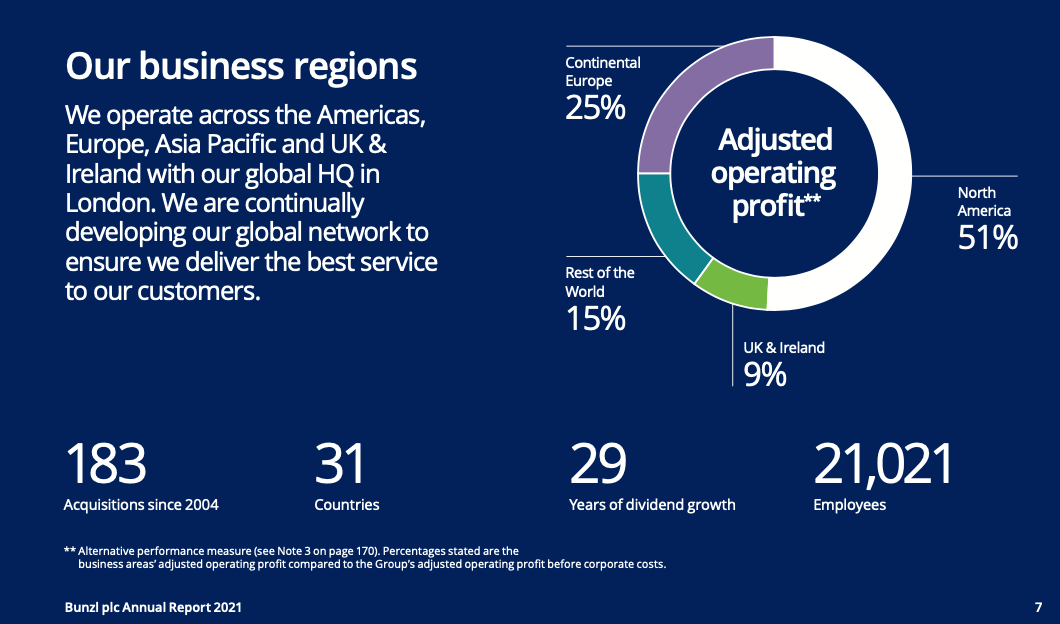

Bunzl, today, is a specialist international distribution and services Group with operations across the Americas, Europe, Asia Pacific and UK & Ireland. Bunzl provides one-stop-shop, on-time and in-full specialist distribution service across 31 countries, supplying a broad range of internationally and responsibly sourced non-food products to a variety of market sectors, including Foodservice (28%), Grocery (26%), Safety (15%), Cleaning & Hygeine (10%), Retail (10%), Healthcare (8%) and Others.

Foodservice segment focuses on Non-food consumables, including food packaging, disposable tableware, guest amenities, catering equipment, agricultural supplies, cleaning and hygiene products and safety items, to hotels, restaurants, contract caterers, food processors, commercial growers and the leisure sector, while Grocery is all about Goods-not-for-resale, including food packaging, films, labels, cleaning and hygiene supplies and personal protection equipment to grocery stores, supermarkets and convenience stores.

North America produced about 51% of the profits, with further 33% produced from across Europe with the rest from a splattering of countries.

Acquisition Strategy

Bunzl is a master of the “bolt-on” acquisition strategy1. Since 2004, the group has completed 183 acquisitions. In the five years to 2021, the average size of a Bunzl deal has been £40mn.

These small acquisitions might seem inconsequential, but this strategy has been lucrative for Bunzl shareholders. Organic annual revenue growth has averaged only 2.5% over the last 10 years - roughly in line with broader economic growth. Bolt-on acquisitions, however, provide a value-added boost to growth - increasing the 10 year CAGR to 7.1% after including acquisitions.

From this article:

One benefit of Bunzl’s “think small” strategy is that price discipline is easier when there is a multiplicity of potential vendors. The company, a former maker of cigarette filters which was derided as “Bungle” in unhappier times, has typically paid between 6-8 times ebitda. It has maintained that throughout the cycle.

Bolt-on deals also have the advantage that they can be systematised. The purchaser establishes a routine of buying up smaller competitors, integrating them and cutting costs to raise margins.

and again from there:

The result is a healthy 19 per cent average return on capital invested. This is comfortably ahead of the group’s weighted average cost of capital of 6-8 per cent. As a result, Bunzl shares have returned 225 per cent over the past decade and have comfortably outperformed the FTSE All-Share index. Discipline is needed to maintain this performance.

What is interesting about the acquisition strategy is that it has worked even during the past 10+ years when asset prices of every asset have been on the rise due to the low-interest-rate regime we have lived through. With interest rates like to remain structurally high, many targets’ crowdedness might come down and will likely favour Bunzl.

From their annual report:

The 14 acquisitions made in 2021 are complementary to our existing businesses and demonstrate the quality of acquisition opportunities in the pipeline, as well as the breadth of opportunity, with acquisitions made across all of our business areas.

It isn’t also trying to just build an empire through acquisitions. Where sensible, it is willing to offload business units, in order to focus on opportunities with the best forward looking return - for instance, in 2022, Bunzl sold its UK Healthcare division to fund new investments.

Despite all the acquisition, the balance sheet remains solid, with a current ratio of 1.33, and a total ratio of 1.45.

Business Metrics

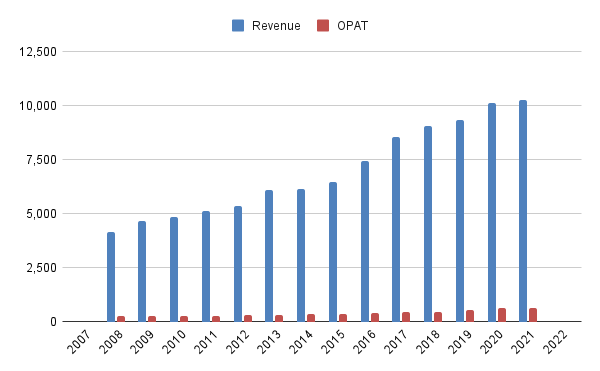

For what I would call as a boring business, the consistency of their business growth is remarkable - over the past 13 years, revenue has grown 7.18% p.a., and OPAT 7.46% p.a.

Over the past 3 years, Bunzl has done well to make the most of Covid-19, where some segments saw new demand that filled the hole in the base business in 2020, largely reversing itself since 2021. Management sees Safety & Cleaning & Hygiene as two categories with most revenue growth opportunity.

Acquisitions have not cost the shareholders any noticeable dilution. Cashflow has been up and down over the years, mostly due to investments taking away cashflow as and when they happen, however, company maintains a healthy cash and cash equivalents balance in most years.

From their annual report on cash conversion:

Cash conversion (operating cash flow as a percentage of lease adjusted operating profit) remained strong over the year at 102%. The Group’s cash generation continues to be impressive, with £525.4 million of free cash flow generated in 2021, representing 15.0% growth at actual exchange rates compared to 2019, and continuing to enable strong investment in the business and acquisitions.

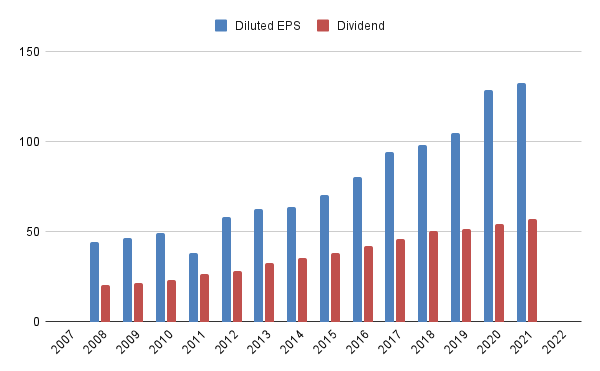

Diluted EPS has been growing at 8.77% during the period, and accordingly, the management has paid back ever increasing dividends, growing at 8.14% during the period. 2023 will be the 30th consecutive year of sustainable dividend growth for the company.

From their latest annual report:

Since 2004 Bunzl has returned £1.8 billion to shareholders through dividends and has committed £4.4 billion in acquisitions to support a growth strategy that has delivered an adjusted earnings per share compound annual growth rate of 10% over the period.

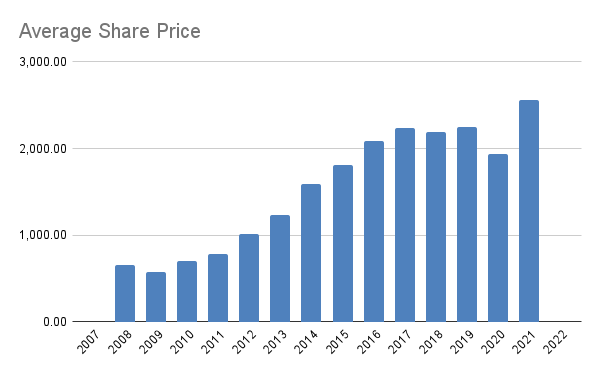

Share price has reacted to all this good news, growing by about 11.12% during the intervening period.

This is a staid but consistent business that is put one particular advantage - bolt on acquisitions - to good use to leverage their returns. On the surface, nothing not to like.

The only problem with the stock is that it is not cheap. It normally trades around the 20 P/E mark, and has consistently traded between 18-30x P/E over the past 10+ years. The last time you could get hold of this business relatively cheaply (<15x P/E) was before 2012. So, the market realises the strength of the business and is willing to accord it the respect, but leaves little margin of safety for the new buyer.

Acquisition Target

Given how this business is run, and their relatively small size, I wouldn’t be too surprised to see Bunzl itself being a target for acquisition by a big player. In my humble opinion, being taken private, or acquired by a larger listed company rates is a 50-50 outcome over the next 10 years.

At £10B market cap, they aren’t too big for most buyers, and aren’t too small, even for a buyer like Berkshire Hathway (or countless others like them) to get considered. I hope that current shareholders can get a reasonable outcome when that happens.

Risks

Inflation on the inputs and deflation on sales are obviously a very important risk factor for this company, specially under competitive pressures. So, maintaining a healthy supply chain and prudence on its cost will be an important imperative for the management and something to keep an eye on.

More importantly, a company that focuses so much on acquisitions could easily fall prey to a bunch of conditions that could be a major distraction for the board and management:

Deals can get costlier when more buyers crowd around assets.

Deals can go sour, dragging Bunzl into litigations. If one of them happen at a time, it is probably manageable, but if multiple happen at the same time, it could prove messy.

The temptation to veer off the course of bolt-on acquisitions and go into a big acquisition that they falter upon is ever-present, specially if there is a change of guard in management. Keep a look out for this one.

Taxation - UK is going to increase corporate tax rates from 19% to 25% which would obviously mean less profits for reinvestment and for shareholders. Effective tax rate is 22.3% as of 2021, but expected to rise to 24-25% by 2023-24.

A business that presents good results with this consistency, even if the results are only moderate, should also be viewed with the lens of “too good to be true”. It could either be that management is using financial jugglery (like GE did for years) or possibly outright fraud (think Patisserie Valerie). To be clear, there is no evidence2 to indicate such a possibility and I am definitely not alleging management is involved in anything of the sorts, but I wouldn’t have an heart attack if I wake up to news of the kind.

Do I expect any one of these risks to happen? No, but risks must be called out objectively.

Do you see other risks? Add a comment please.

Latest on Bunzl

Bunzl has not yet reported full year 2022 numbers. However, in an October trading statement, management guided to a 10% YoY increase in revenue on constant-currency basis (and 17% on absolute basis, as they have largely traded in currencies stronger than GBP while reports are published in GBP), so the business continues to do well beyond the pandemic rush it received in its healthcare business, and despite of challenging macro-economic conditions of the past 12 months.

Summary

In summary, Bunzl’s business activities in sectors not covered by my portfolio otherwise, and its niche in bolt-on acquisition based growth, provide welcome additions to my Coffee Can Portfolio. It is a bit costlier than I would like it to be, but given its consistent track record and its conservative capital allocation and dividend policy, I feel comfortable owning this stock for the long term. If the story doesn’t change, and if it gets materially cheaper due to market events, I might pile on the stock. Otherwise, I plan to build my position slowly and steadily during the life time of my coffee can portfolio.

Programming Note: This substack has its own Twitter handle now - @coffeecaninvstr. Please follow it and share it with your investor friends.

Disclaimer: I hold positions in all the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Reference & Inspiration: https://www.businesstelegraph.co.uk/bolt-on-takeovers-are-better-than-betting-the-ranch/

Bunzl’s last annual report was signed off by PWC, so no red signal there, but as we all know, being audited by a Big-4 doesn’t accord much comfort.