Summary Analysis: BAE Systems

A safe bet on increased defence spending

Today, I am going to write briefly about BAE systems (LON:BA). It is one of the best performing stocks in my Coffee Can Portfolio with an IRR of about 38% as I entered it just before it inflected in recent months.

BAE Systems as it is known today was officially formed in 1999 through the merger of two major British defense companies: British Aerospace1 (BAe) and Marconi Electronic Systems. The merger resulted in the creation of BAE Systems plc. BAe was originally a publicly owned company before being privatized in 1981, during the Margaret Thatcher era, floating 51% of the shares in an IPO. This marked the transition of British Aerospace from a government-owned entity to a publicly listed company on the London Stock Exchange. After the merger with Marconi in 1999, we get to the current state of the company.

Presently, BAE is a multinational arms, security and aerospace behemoth, based out of the UK. It is the biggest manufacturer in Britain as of 2017. It is the largest defence contractor in Europe and the seventh-largest in the world2.

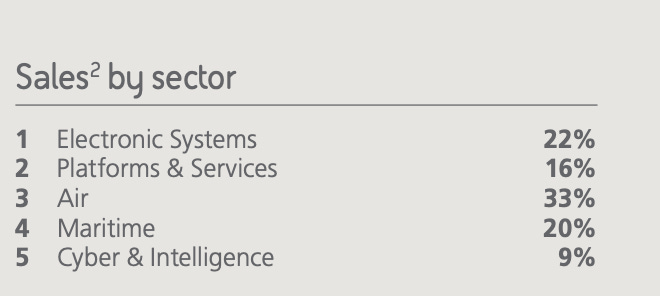

The company operates in 5 different business segments, with Air being the largest, Cyber and Intelligence the newest, and Electronic Systems, Platforms & Services and Maritime accounting for the rest of the revenue.

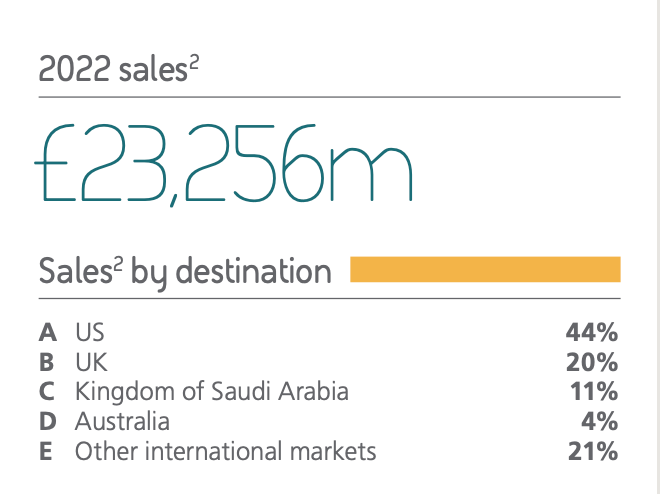

In terms of regional split, US and UK form about 2/3rds of the sales with the rest coming from a splattering of other markets.

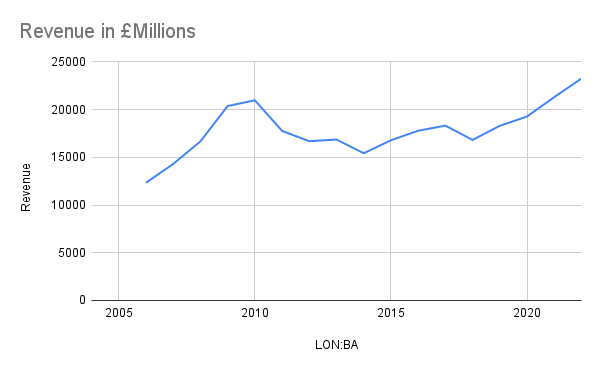

If one rolled back 15 years, selling arms and security apparatus in the developed world has not been a super exciting business for a while as we have gone through a period of relative peace (after perhaps the Iraq and Afghanistan wars) and fiscal reduction in defence budgets.

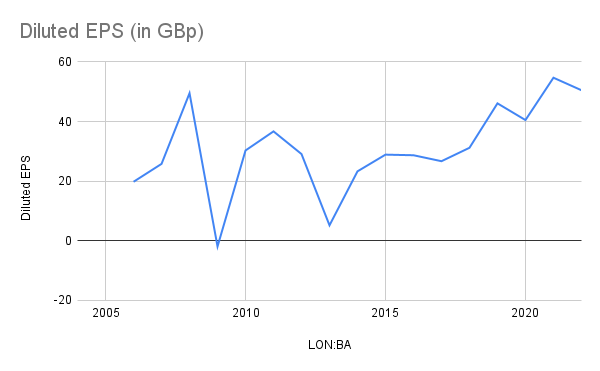

This has reflected in what has been an era where BAE revenues have been up and down.

EPS has been up and down too.

However, in the recent years, the company has shown some consistency, specifically since Charles Woodburn took over the CEO position at the company in 2017, from whence revenues and EPS have both been on a steadier growth upwards. His performance at BAE is considered august enough that some BP investors want him to be running BP instead of BAE. One of the risks naturally then is whether the company will suffer some slowdown is Woodburn were to leave.

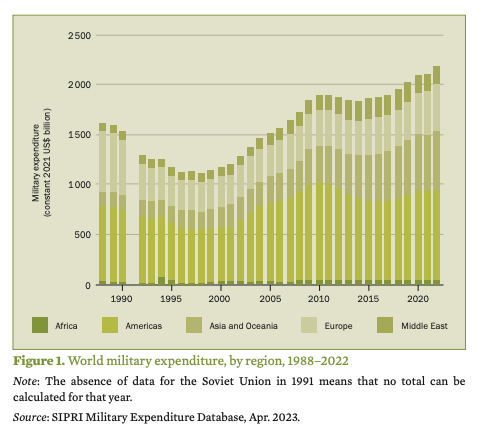

As investors, we must hope for a peaceful world, as it benefits both humanity as for us as investors - peace dividend is a real phenomenon. However, peace in the world goes hand-in-hand with self-defence, which is precisely the world BAE systems operates in. With the recent Russian-Ukraine and Israel-Hamas wars, spending on defence is expected to inflect upwards3.

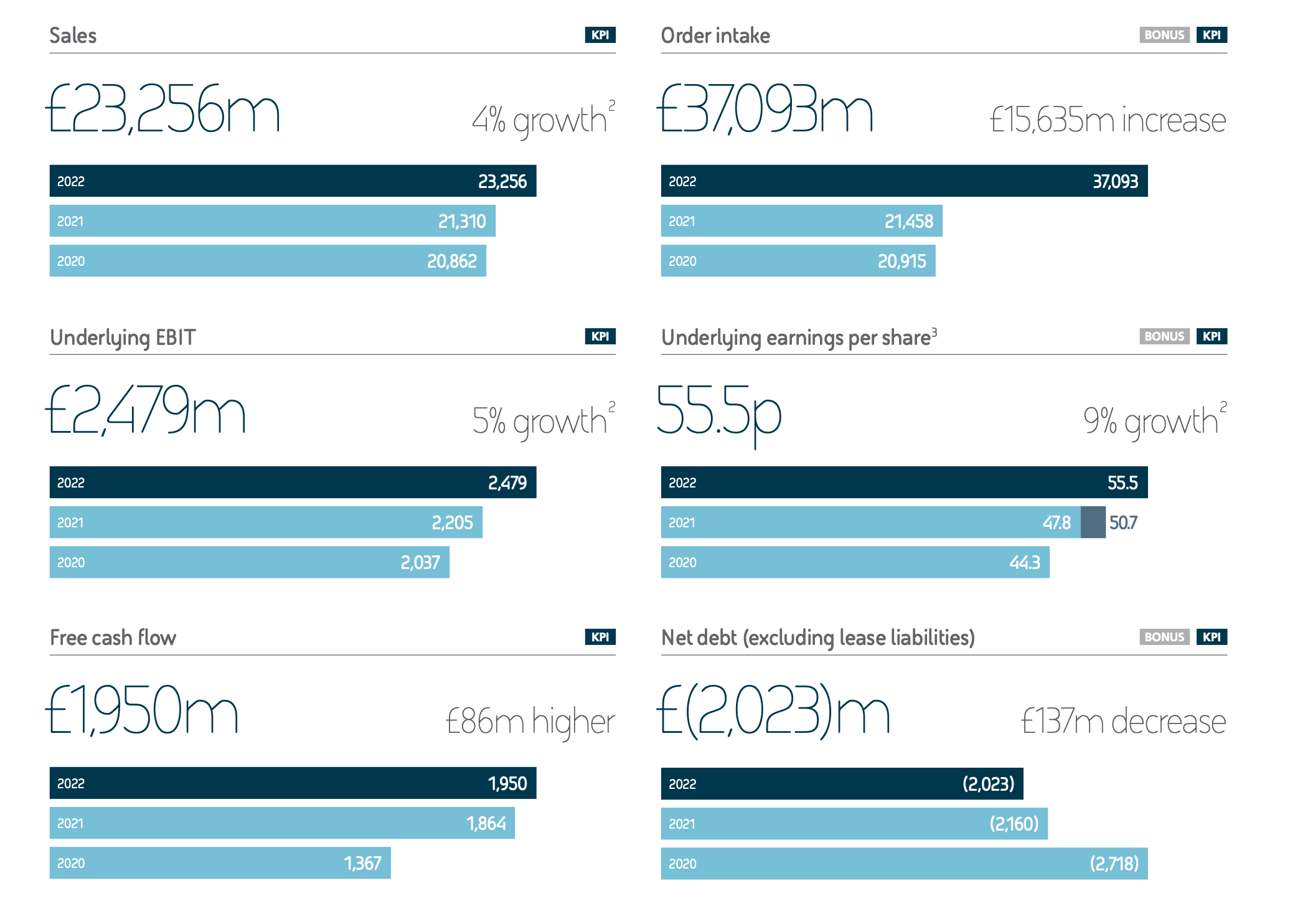

I am not an expert in military spending or even in geopolitics, so I won’t offer too much of a view here, except that it is worth looking at some numbers. Look at BAE Systems’ backlog for example, which moved from circa £45Bn in 2019 & 2020 to now being £66Bn, which against the backdrop of the fact that BAE system delivers only about £20Bn-£23Bn of revenue per year, reflects an entire additional year of backlog. Essentially the world has gone from ordering 2.2 years of service in advance to now ordering 3.3 years in advance, which is a massive tailwind for the company.

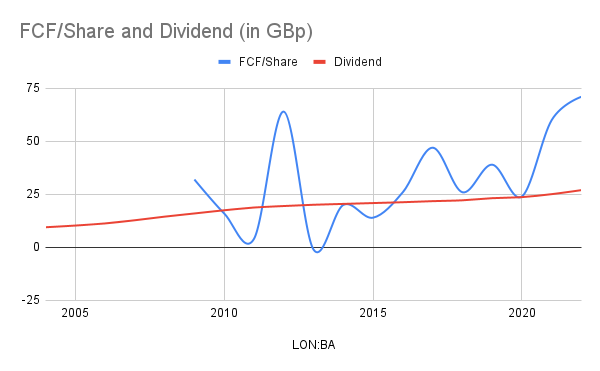

Combine this with a company that has proven itself very good at generating Free Cash Flow and pass it on to investors in the form of an evern increasing dividend. Dividend today stands at 2.38%, but is well covered by FCF (2.5x) as well as EPS (2x).

Today, this company can be purchased at 18.94x earnings (16.6x FCF) , which given the fact that it is a (a) well run company (b) with a track record of cash generation (c ) investor returns through dividends and (d) revenue tailwinds means that it is a relative safe bet on future cash returns. Obviously, I would like to have acquired a lot more when it was trading in £7-£8 range after the Russian-Ukraine war was already underway, but even at the ~£11.8 price range today, it doesn’t look too bad. A look at few of its competitors like Lockheed Martin and Northrop Grumman tells you that in terms of pricing, they are all comparable, with BAE systems being a clear winner in the last 5 years.

I intend to add to my position from time to time.

As always happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

British Aerospace itself had been formed in 1977 through the nationalization and merger of several British aerospace and defense companies.

based on 2021 revenues.

As a simple example: "Now is the time for all allied and democratic nations across the world to ensure their defense spending is growing," U.K. Defense Secretary Grant Shapps declared at the Lancaster House in London. "Because, as discussed, the era of the peace dividend is over. In five years' time, we could be looking at multiple theaters involving Russia, China, Iran and North Korea." As a result, Britain will be sending some 20,000 personnel to lead NATO's latest Exercise Steadfast Defender, marking one of military alliance's largest deployments since the end of the Cold War.