JISA: Just Incredibly Sensible Actually

The UK’s Unsung Hero for Future-Proofing Your Child’s Finances

Among the many quirks of the UK tax system - where acronyms abound and financial jargon flows freely - there’s one savings instrument that, in my opinion, quietly stands out as the winner for parents: the humble Junior ISA, or JISA.

Now, if you're new to the alphabet soup of UK saving vehicles - SIPP, ISA, LISA, JISA, EIS, SEIS, VCT - you could be forgiven for thinking you’ve stumbled into a Scrabble championship. But the JISA, tucked in there without much fanfare, might just be the best-kept secret for future-proofing your child’s financial life.

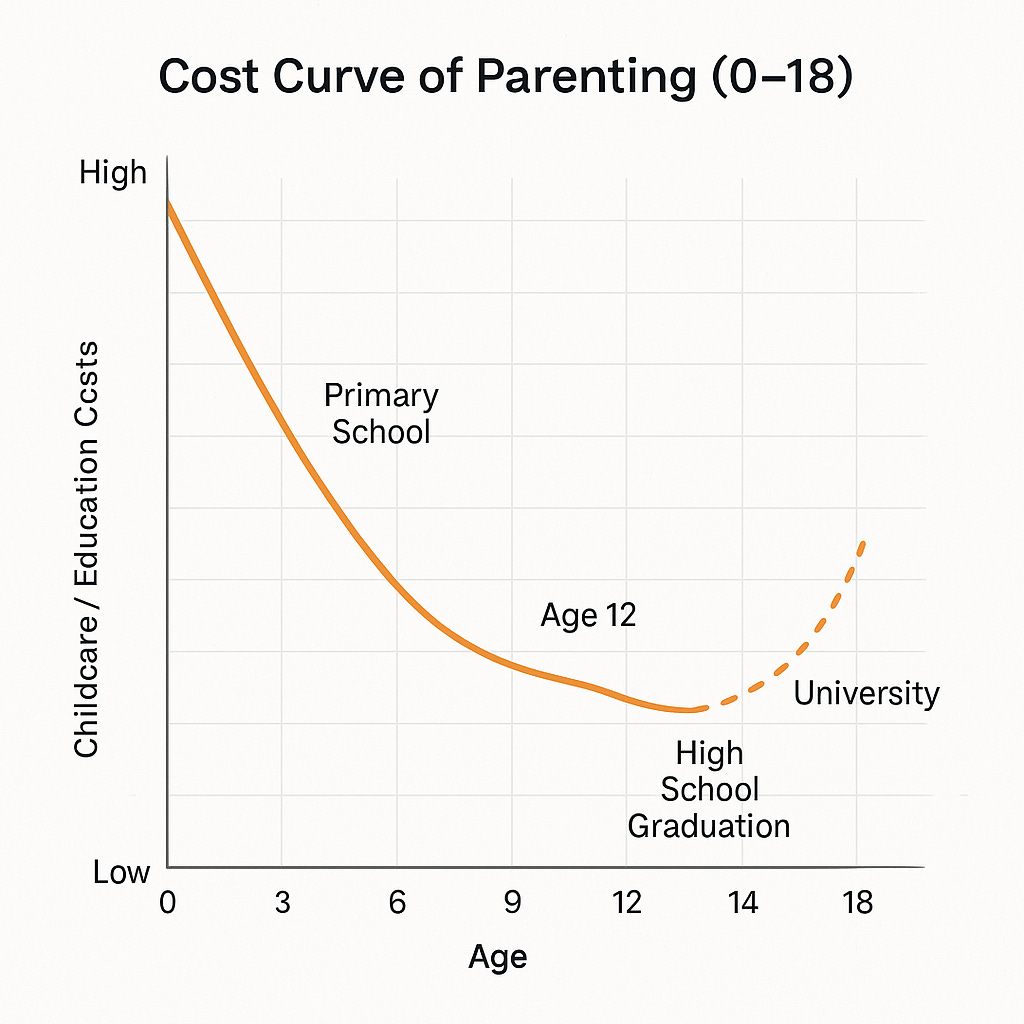

A (Slightly Bumpy) Parenting Cost Curve

Let’s take a step back. Parenting in the UK comes with its fair share of costs as well as drama. The early childcare years can be brutal, both emotionally and financially. Between nursery fees and wraparound care, many families find themselves squeezed.

But things improve dramatically when your child hits primary school around age five. Suddenly, childcare expenses drop off a cliff. Babysitters become optional, after-school clubs are affordable, and by the time your kid is 12 and legally okay to be left home alone (for short spells), those costs are nearly gone altogether.

And then - bam! Just when you’ve relaxed a little, university looms.

While the UK’s student loan system isn’t perfect, it’s fairly generous and income-based. I’m quite likely to encourage my daughter to make use of it. That said, not all paths are linear. What if she wants to study abroad? Or pursue an unconventional path into adulthood? This is where the JISA shines - as a flexible financial cushion that doesn’t rely on state support or parental cash flow when it’s least convenient.

So, What Is a JISA?

Glad you asked.

A Junior ISA is a long-term, tax-free savings account for children under 18, with an annual contribution limit of £9,000 (up from £4,500 when we first arrived in the UK). You can invest cash, stocks, or both - and once the money’s in, it grows tax-free until your child turns 18.

If you fully fund a JISA every year from birth to adulthood, you’re potentially handing your child a six-figure head start. Even contributing half the annual limit, if invested smartly, can cover a substantial portion of a UK university education.

Because the money is locked away until your child reaches 18, the JISA nudges you toward long-term investing, which tends to yield better returns. With no temptation to dip in for a new car or home repair, you're more likely to invest it in productive, growth-oriented funds.

But What If They Blow It?

A common concern is that once your child turns 18, that money is legally theirs. You lose all control. What if they blow it on something reckless?

That’s a fair worry. But honestly, if your child isn’t equipped to handle a lump sum responsibly at 18, the issue isn’t the JISA - it’s a parenting challenge. Whether the funds come from an education loan, your own pocket, or a JISA, the important work is teaching your child financial literacy, values, and decision-making.

In our case, the JISA isn’t where we started our financial planning for her - we started by having candid conversations about money. We discuss the trade-offs we make at home, including the choice of her secondary school (private vs state and why we chose state) and our many other choices. Is it guaranteed to work? No, but I consider coaching her on money a higher priority outcome that handing her any money. On that neither my wife nor I have any doubts.

Our Family’s JISA Journey

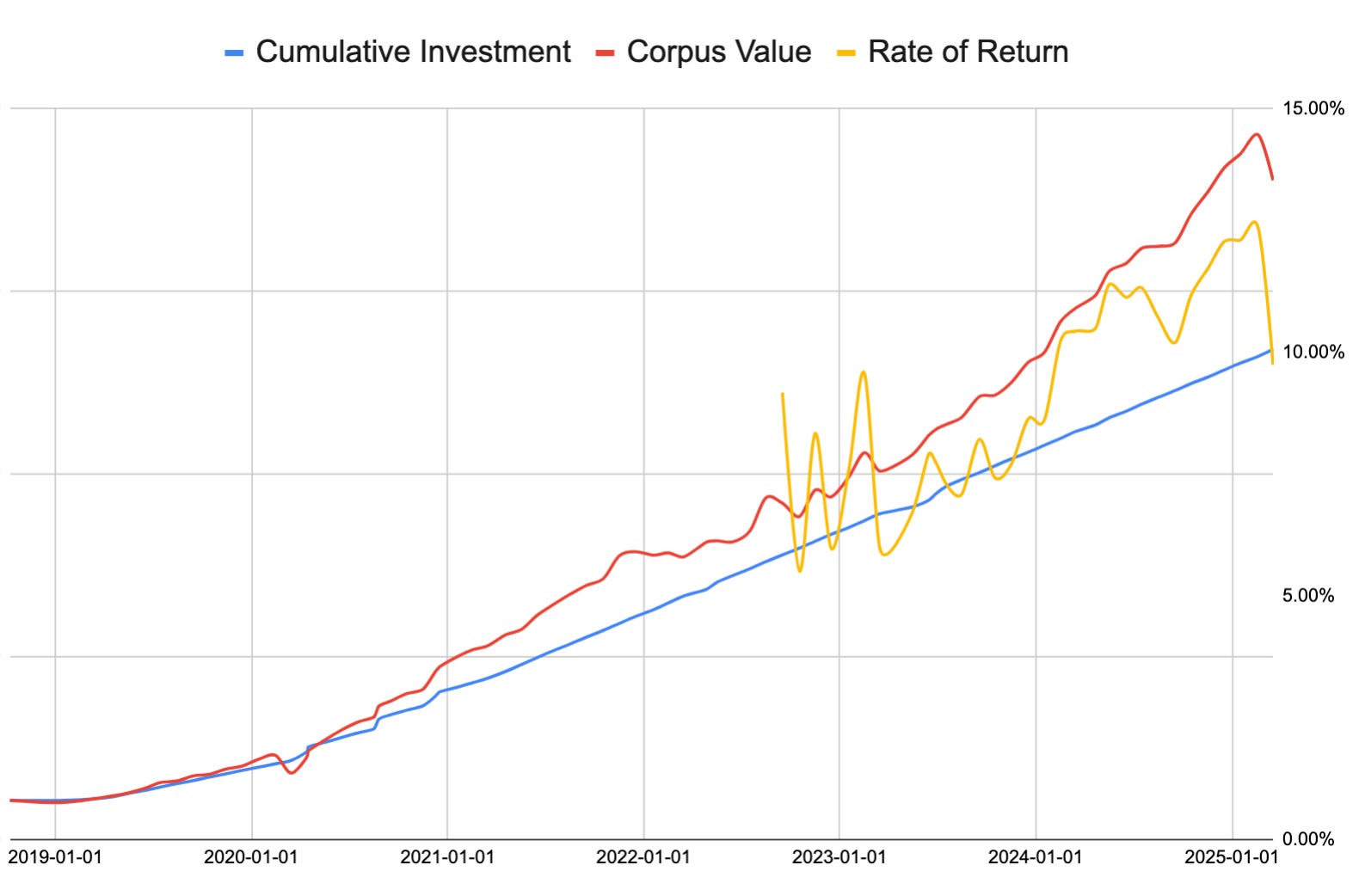

When we moved to the UK in 2018, our daughter was six years old. From October that year, we began diligently putting away money into her JISA. We opted for a simple, broad-based investment strategy: the FTSE Global All Cap Index fund.

Every pound has gone into that one fund. The average purchase price per unit is £163. As of this writing, each unit is valued at £222.92 - a solid return, built quietly over time. We didn’t try to time the market, we didn’t get fancy. We just invested regularly and stayed the course. Boring? Maybe. Effective? Absolutely.

In fact, we’ve prioritised our daughter’s JISA even over funding our own ISAs or pension accounts. Why? Because her university education will come long before our retirement - and it’s the next big financial milestone we’re working towards.

And If She Doesn’t Use It for University?

All the better! If she doesn’t need it for higher education, then the money becomes the starting point for her own adult ISA journey. She’ll have a head-start on saving for a home, a business, a sabbatical, or whatever dreams she might chase in her twenties.

Final Thoughts

In the grand scheme of UK personal finance, I think the Junior ISA is one of the most elegant and well-designed tools out there. If you’re a parent and your child is under 18, it’s a no-brainer to take advantage of it. It’s not just a savings vehicle - it’s an investment in your child’s future, both financially and emotionally.

Happy investing (for your children)!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.