Harley-Davidson (NYSE:HOG) Q3 Review

Between Legacy Trouble and Financial Engineering

Harley-Davidson (NYSE:HOG) reported its third-quarter results this week. Since it’s one of my largest individual holdings (behind only Berkshire), it’s worth taking a close look at where things stand.

For a company trading at $27 before earnings, posting nearly one-ninth of that in quarterly EPS should have pushed the stock higher.

Instead, it dropped. Let’s unpack what’s really happening under the hood.

HDMC – The Core Business in Decline

At its heart, Harley-Davidson builds and sells motorcycles, along with apparel. This remains the company’s troubled core. Unit sales have been falling for at least 11 straight quarters, dragging revenue down each time. It’s been a slow-motion contraction that shows little sign of reversing.

The company’s attempt to enter the EV segment through its LiveWire brand has fared no better. Losses continue to mount, reaching $18 million in the latest quarter, with revenue flat.

With the seasonally strong quarters now behind us and Q4 likely to come in soft, HDMC will probably deliver no more than $150 million in operating income for the year. That’s an optimistic estimate.

HDFS – The Transformation Story

Harley-Davidson Financial Services (HDFS), the financing arm that helps customers buy its bikes, tells a more complex story. This segment has been a steady profit generator, but it is now in the midst of a structural shift.

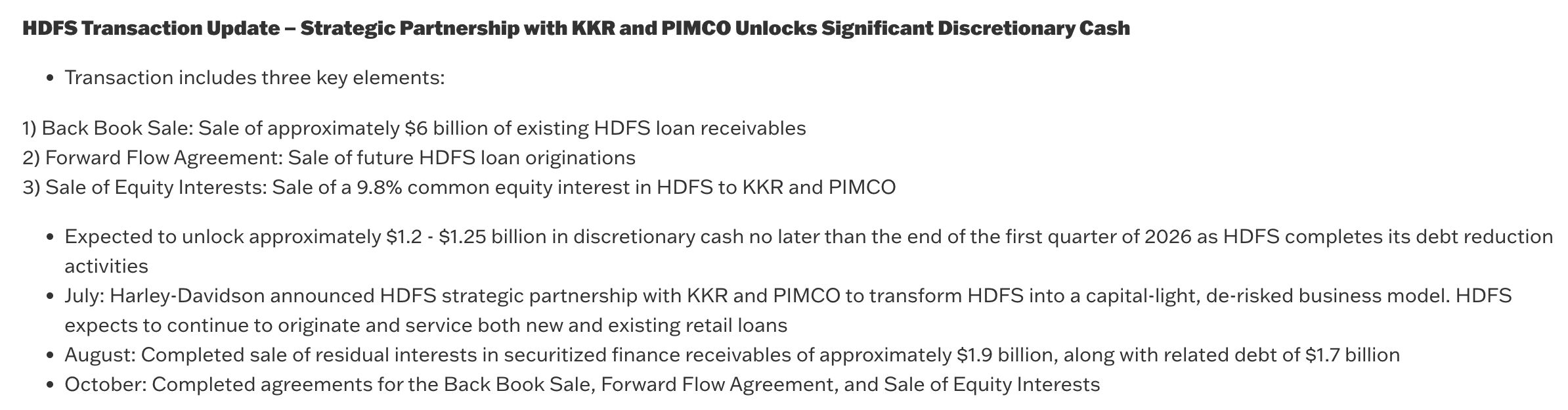

Historically, HDFS both originated and held loans, funding its portfolio by borrowing heavily from the market. This model left the company carrying significant debt and credit risk. That changed earlier this year when Harley-Davidson transferred all loan originations - and the existing loan book - to a consortium led by KKR and PIMCO.

With that move, the company released $327 million in loan-loss provisions in Q3 alone, inflating the quarterly profits. These are paper gains, not cash. The real benefit comes next: as the deal closes fully between Q4 and Q1, Harley-Davidson will unlock about $1.2 to $1.5 billion in cash.

Future loans will be underwritten by the partners, removing the need for the company to issue debt or maintain loss provisions. The trade-off is lower margins per loan and the sale of a 10% stake in HDFS to its new partners.

Once the transition settles, HDFS should stabilize around $260 million in quarterly revenue and $25–30 million in operating income, of which Harley-Davidson will keep 90%. A smaller, cleaner, capital-light business.

Capital Allocation – The Bright Spot

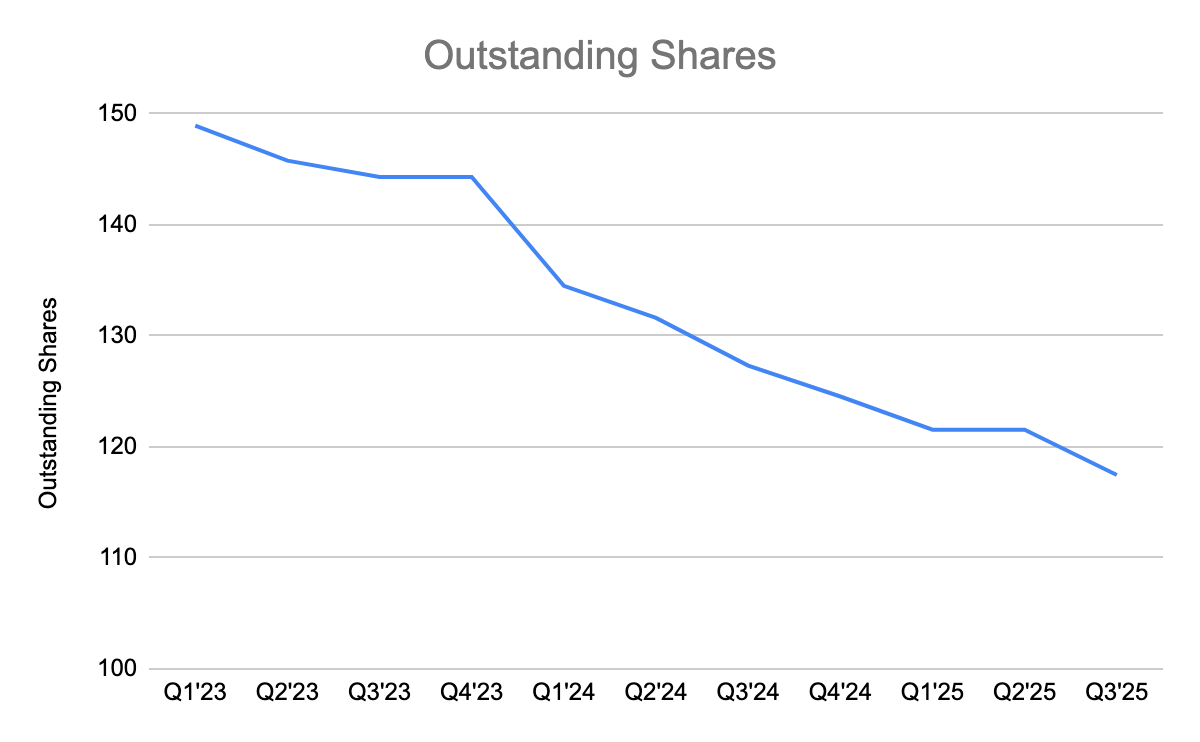

This is where management has shown discipline. Over the past 11 quarters, Harley has retired about 30 million shares, roughly 20% of its outstanding stock. With the influx of cash from the HDFS transaction, buybacks are set to accelerate.

Of the $1 billion repurchase authorization, only $194 million has been used so far. Another $200 million will go toward an accelerated share repurchase from Goldman Sachs by early 2026, leaving roughly $600 million still available. If all of this is deployed, the share count could drop from 148 million at the end of 2022 to around 90–95 million - a dramatic reduction. Even after these buybacks, Harley should still hold about $2 billion in cash and roughly $3 billion in retained earnings.

Valuation – The Push and Pull

After several passes through the numbers and a few spreadsheet recalculations, here’s how the picture looks by mid-2026:

HDMC generating around $150 million in annual operating income

A capital-light HDFS contributing about $100 million

Free cash flow in the range of $250 million

Around 95 million shares outstanding

That suggests forward EPS of roughly $2.60. At $25 per share, the stock trades just under 10 times earnings.

Is it cheap? Not really. A shrinking core business with an uncertain turnaround doesn’t deserve a premium multiple. The risk is clear: continued decline in motorcycle sales could drag the stock lower.

But the bull case is equally clear. If sales stabilize or inflect upward, the market will rerate quickly. With $600 million still earmarked for buybacks against a post-deal market cap of about $2.9 billion, the share count reduction alone could move the stock.

It’s not an easy story to own. If I came across this business fresh, the core numbers would probably make me pass. Yet having followed it closely and seen the balance sheet improvements, I’ll stay on board for another quarter or two. If either side of the thesis plays out - let alone both - it could be a rewarding hold.

With that note, Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.