2025 - A Boring Year for Indian Equities

And why that's the opportunity

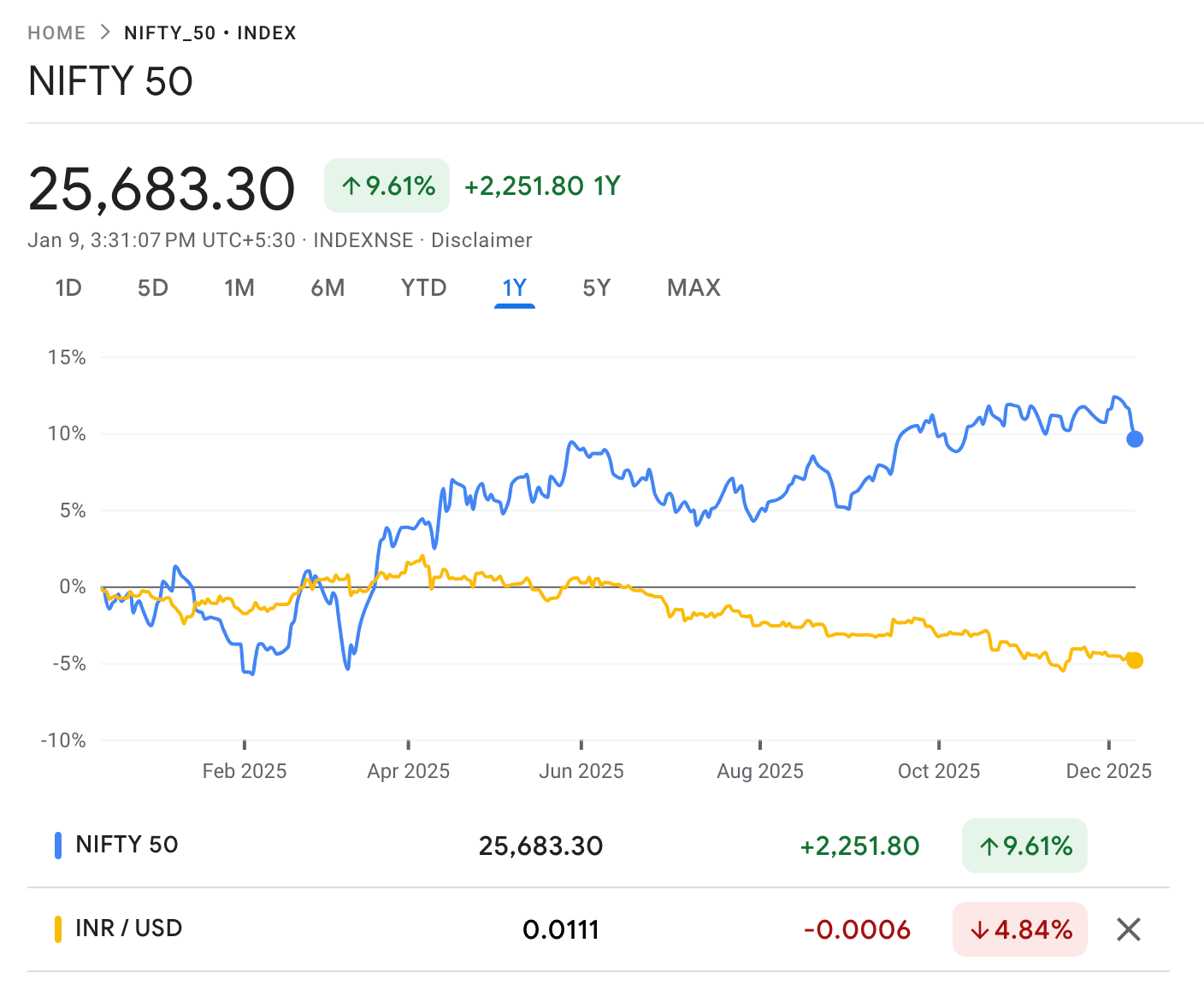

2025 was a poor year for Indian markets, underperforming global markets by an extremely high margin. In INR terms, indices went sideways but add sharp rupee depreciation, you get a rather bleak picture.

Foreign investors sold aggressively, while gold, the Indian equity investor’s primarily competitor, had a stellar year. And yet, at the macro level, the picture looks different. The Indian economy, by most measures that actually matter, continued to hum along just fine.

This divergence - between a relatively dull equity market and a still-strong underlying economy - is precisely what makes 2025 interesting. And, perhaps counter-intuitively, what may make it one of the more attractive years to build long-term positions.

Domestic Capital: The Real Story of 2025

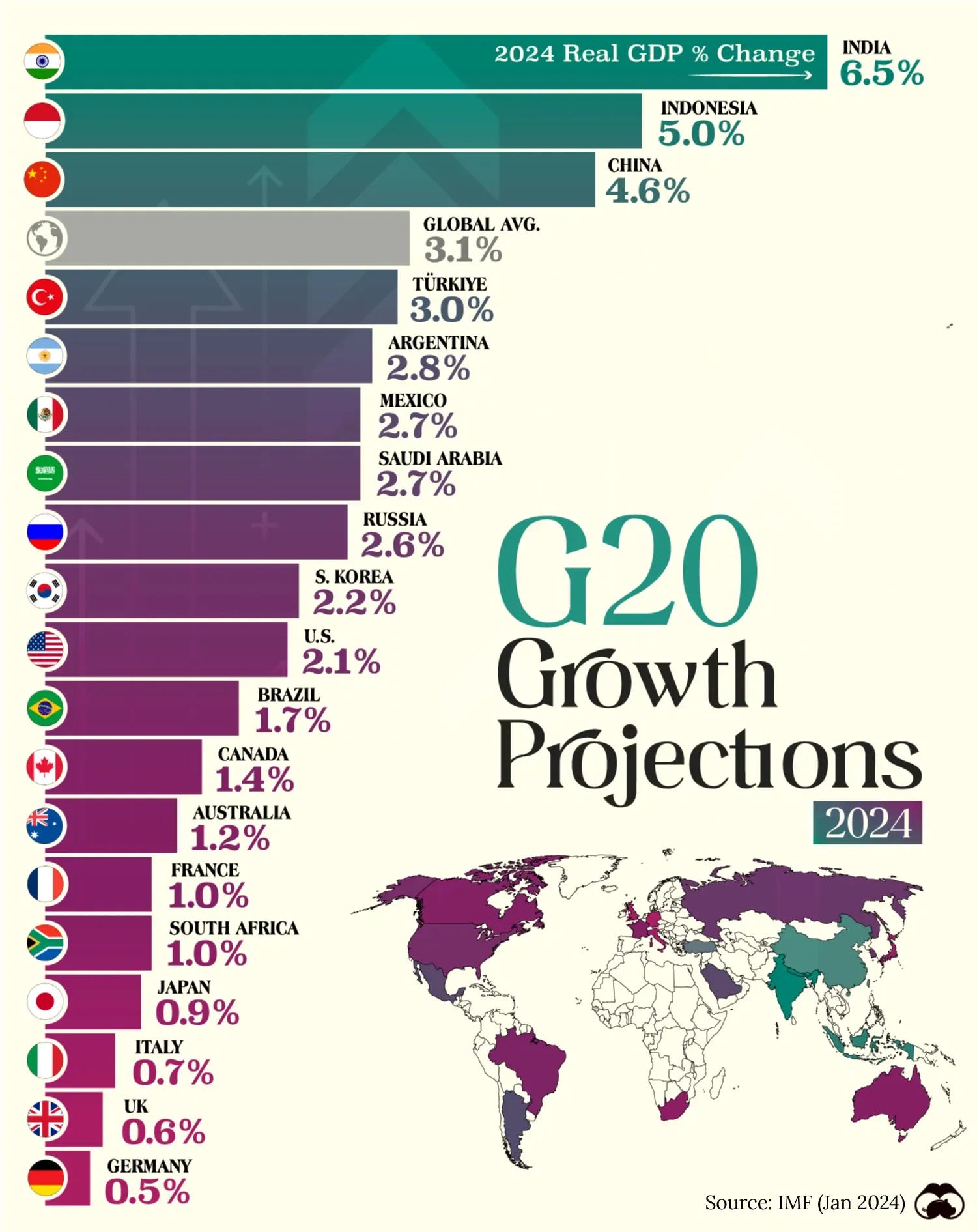

2025, as tepid a year as it was, marked the end of the post-COVID earnings upgrade cycle in Indian markets, which had a spectacular few years. Largely due to a perhaps unfair narrative that India was an “AI loser” - prompting capital rotation into China, Taiwan, and Korea - and India briefly became a funding market. Passive outflows amplified the move as India’s weight in global indices fell. Foreign portfolio investors sold roughly ₹1.5 trillion worth of equities over the year.

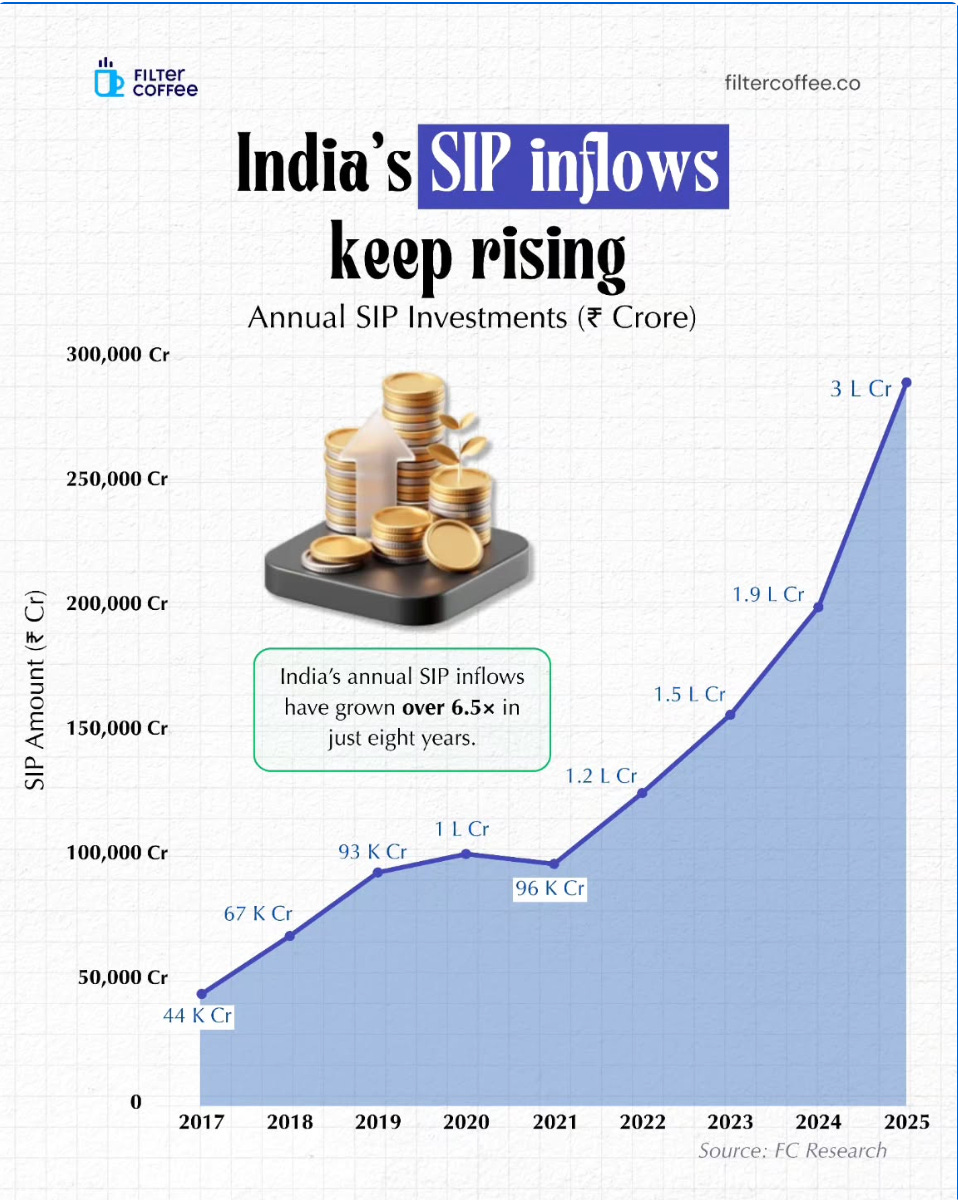

And yet, the indices didn’t collapse. If there was one dominant force holding Indian markets together in 2025, it was domestic capital. Domestic institutional investors, primarily mutual funds funded via SIPs, injected close to ₹3+ trillion. This wasn’t hot money chasing momentum. It was slow, systematic, and largely indifferent to short-term volatility.

This is the quiet revolution that doesn’t get enough airtime. Household savings are being steadily financialised, moving away from real estate and gold and into market-linked instruments. Estimates suggest roughly ₹5 trillion a year now flows into equities via this route (SIP + other investments). Even in a year when gold performed exceptionally well - traditionally a competitor for household savings - equity flows held up.

Now imagine what happens when foreign investors return - not with exuberance, but simply with neutrality.

Fiscal, Financial & Political Strength: An Underappreciated Advantage

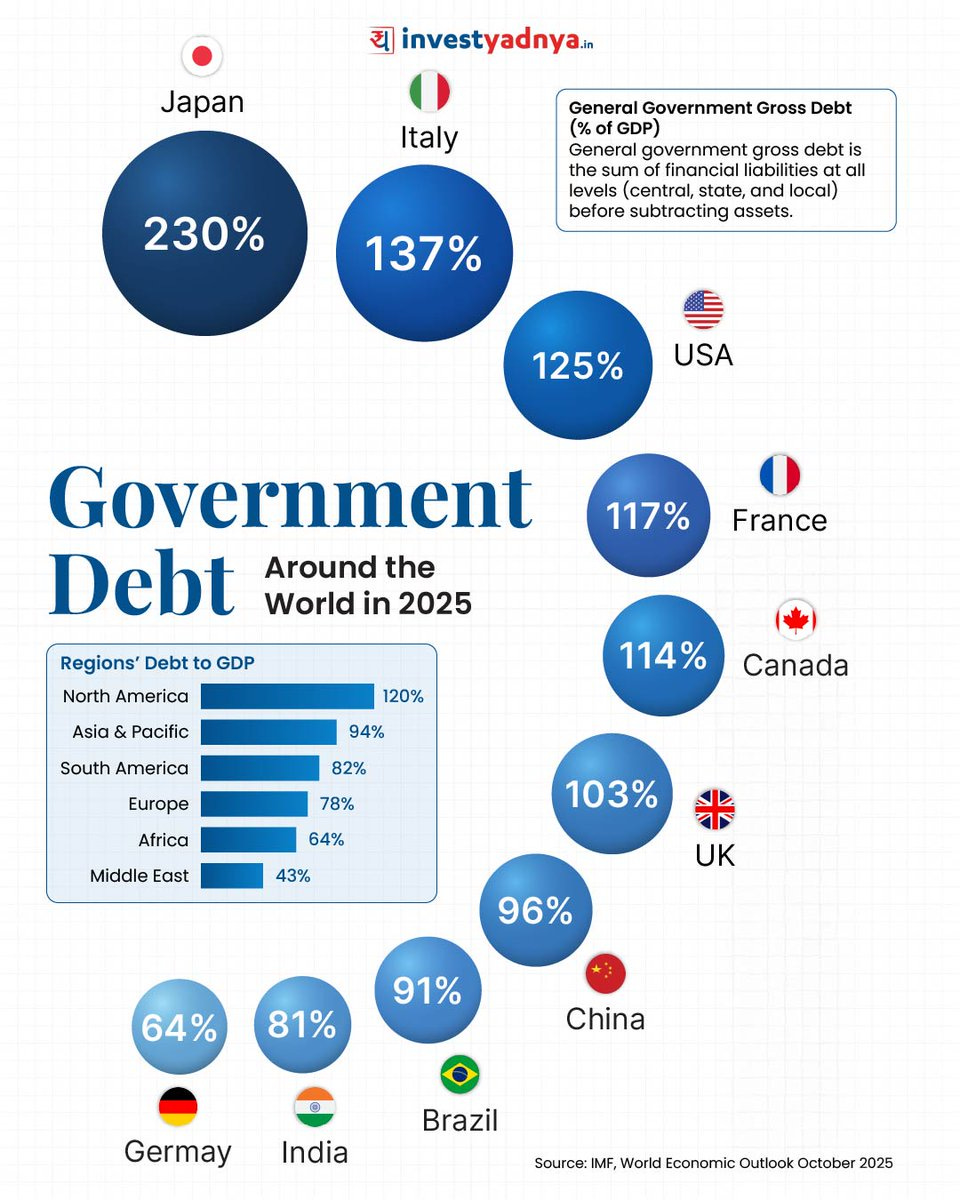

One of India’s most underappreciated strengths remains its balance sheet.

Government debt-to-GDP at 81%, while not trivial, is far more manageable than many developed peers. Remember that due to natural growth and inflation, this is far less cumbersome than at countries with miniscule growth rates.

Household debt sits at roughly 41% of GDP — compared to ~75% in the UK and ~60% in China. When global shocks emerged in the past 12 months - tariffs, trade uncertainty, external volatility - India had room to respond fiscally, and react they did - cutting GST rates between 5% and 12% across many categories.

Contrast that with the UK, where fiscal headroom is so constrained that even modest relief measures feel like political brinkmanship. This matters because fiscal flexibility is not just about stimulus - it’s about optionality, and it seems India both has it and is willing to flex it as required.

As regulators, both the RBI and SEBI deserve credit here - few regulators globally have overseen such a rapid expansion of retail market participation without a corresponding deterioration in stability. The financial system has been nudged - firmly but patiently - towards transparency, discipline, and resilience.

“Mutual Fund Sahi Hai” is a classic example.

India’s political stability is often taken for granted. It shouldn’t be. Since I started my professional career, way back in 2004, India has had two prime ministers. Since the turn of the century, three! The UK saw as many in the calendar year of 2022 alone!

Markets don’t need perfection. They need predictability. India has quietly delivered that.

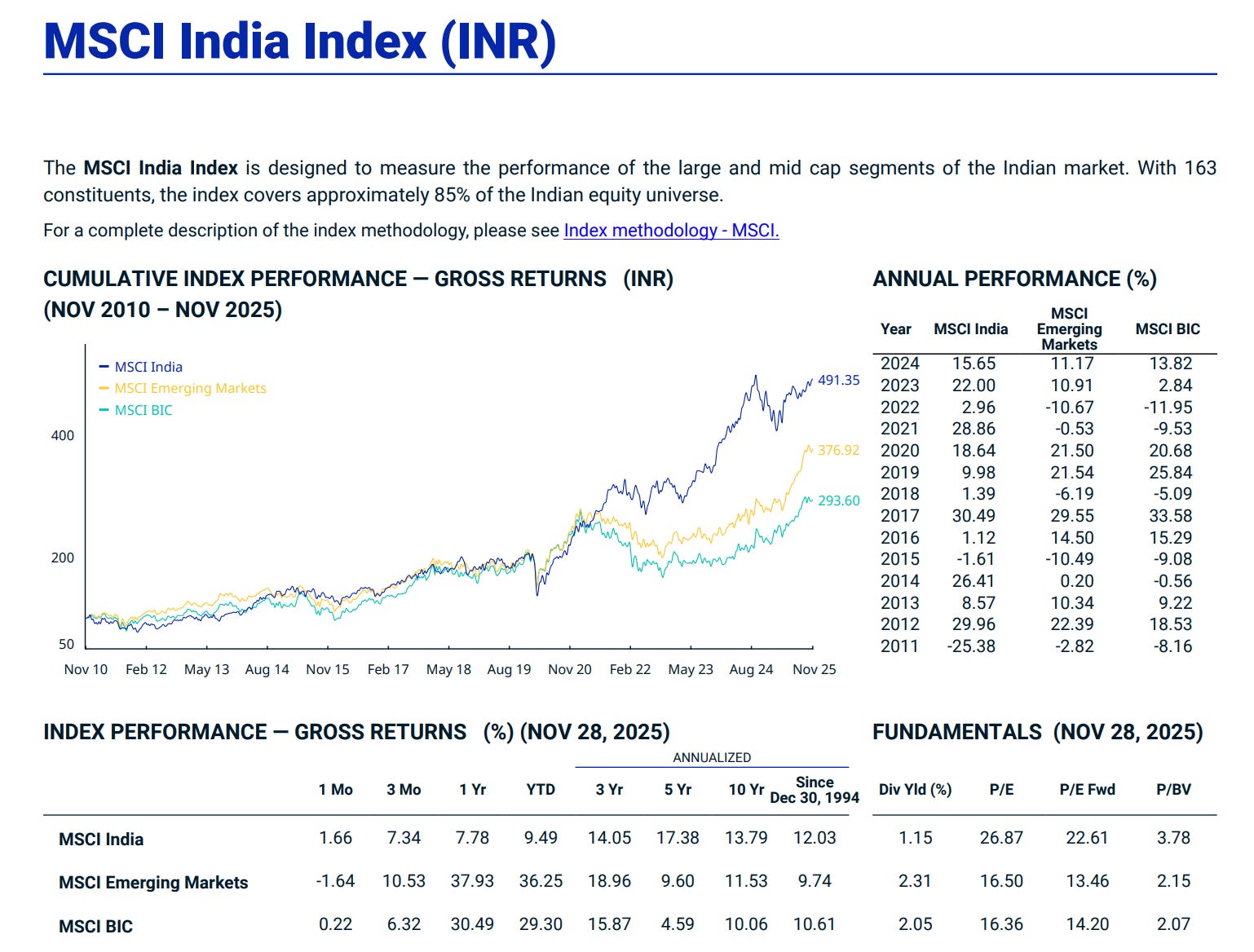

Valuations: Still High, But Context Matters

Yes, Indian equities remain expensive on absolute metrics. That hasn’t changed.

What has changed is the relative picture. India’s valuation premium to global markets - particularly the US - has shrunk to well below its long-term average and is at its lowest level since 2016. Multiple expansion from here may be limited, but the argument that India is egregiously overvalued is weaker than it has been in years.

Meanwhile, long-term fundamentals remain intact. Nominal GDP growth has historically run at 11-12%, combining 6-7% real growth with moderate inflation. Corporate profits tend to grow at least in line with nominal GDP when profit share remains stable.

Add to that a secular decline in the cost of capital - with 10-year bond yields hovering around 6.5% - and you have a market that doesn’t need heroics to deliver reasonable outcomes.

Supply, Demand, and the IPO Deluge

2025 also saw an extraordinary surge in equity supply. IPOs over 2024 and 2025 totalled roughly ₹3.4 trillion - nearly half of all capital raised in the previous 35 years combined. Another ₹3.5 trillion worth of draft papers are already filed.

And yet, the market absorbed it.

With estimated equity demand of ₹5 - ₹7 trillion next year - even without FPI inflows - the supply-demand balance remains supportive. That’s not something India could have said a decade ago.

So Why 2025 Might Matter More Than It Looked

2025 may end up being remembered not as a year of spectacular returns, but as a year of quiet positioning.

Foreign money left. Domestic money stayed. Fundamentals remained largely intact.

I’ve been steadily adding to my India exposure (via LON:IIND ETF) through 2025 - not because it felt obvious, but because it felt available. I will continue to do so given further opportunities in 2026. Markets rarely offer clean entry points when optimism is abundant. They do, however, offer them when boredom sets in.

And boredom, in investing, is often underrated. On that note, Happy Investing!

I was wondering why Indian market wasn’t growing despite being a top 4 GDP growing and fastest growing country in the world. However, I think I overlooked the AI narratives, and geopolitical issues.

Loved your organized thought. ☺️

Nifty 50 seems fairly valued, small caps and mid caps are still above that zone